数学马尔科夫链代写 Math 632代写 Exam代写 数学代写

544Math 632 - Midterm Exam 数学马尔科夫链代写 • There are six problems on the exam, and they have multiple parts. The total number of points is 100. • Your solutions must be fully uploaded • Th...

View detailsSearch the whole station

随机过程考试代考 Each question has several subquestions, whose marks are shown in square brackets. Your answers should be justified by showing your work

Suitable for all candidates

This paper contains FIVE questions (for a total of 100 marks). AnswerALL FIVE.

Question 1: 20 marks

Question 2: 20 marks

Question 3: 28 marks

Question 4: 24 marks

Question 5: 8 marks

Each question has several subquestions, whose marks are shown in square brackets.

Your answers should be justified by showing your work and explaining your steps.

Make sure that your five-digit candidate number and course code are written or included at the top of every page of your answers.

Time allowed: Writing Time:

3 hours

Upload time:

1 hour

Consider a discrete time Markov chain (Xn)n≥0 with infinite state space S = Z. Let the chain be determined by the transition probabilities

p(i, i + 1) = p and p(i, i − 1) = q ∀i ∈ Z,

where p+q = 1 with q < 1/2. Furthermore, let the starting point X0 = i0 < 0 be a negative integer and consider the first time that the Markov chain becomes positive, namely

τ+ := inf{n ≥ 0 : Xn > 0}.

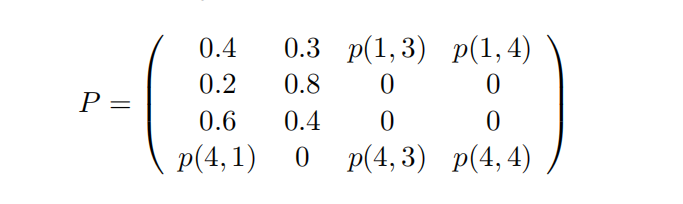

Consider a Markov chain with a finite state space S = {s1, s2, s3, s4}, modelling four different states that your insurance company can be in at the end of the fiscal year. We refer to si as state i. In state 1, things are not so good and your company has made a loss for the year of 1 million pounds. In state 2, your company breaks even, earning precisely 0 pounds. In state 3, things are amazing, earning you 10 million pounds for the year. In state 4, things are also quite good with earnings of 4 million pounds for the year. The transitions between the states are modelled by the transition matrix

If you find it helpful, you are welcome to use drawings to justify your answers. However, it is also fine to just refer to the entries of the transition matrix.

Suppose p(1, 4) = 0 and p(4, 1) = p(4, 4) = 0.4. What are then the values of p(1, 3) and p(4, 3)?

(b) [5 marks] In the setting of (a), identify the closed communication classes, the transient states, and the recurrent states. Briefly explain your reasoning in deducing these clasifications. Is the Markov chain irreducible? 随机过程考试代考

(c) [5 marks] Now suppose instead that p(1, 4) = 0.2 while p(4, 1) = p(4, 3) = 0. How do your answers to (b) change? Again, you should briefly explain how you arrive at the different clasifications.

(d) [5 marks] Finally, consider P with p(1, 4) = 0.2 and p(4, 1) = p(4, 4) = 0.4. Recalling that every finite Markov chain has a stationary distribution π, you may use that

π = (0.3, 0.55, 0.05, 0.1)

is a stationary distribution for this transition matrix P. Write down what it means that this π is a stationary distribution. Explain, by appealing to a theorem from lectures, why these probabilities can in fact be interpreted as the long-run probabilities of being in states 1, 2, 3, and 4, respectively (you need to brieflfly justify why the theorem can be applied). Explain whether or not the theorem applies in (b) and (c).

(e) [4 marks] Let P be as in (d). In the long run, how often do you expect to be making 10 million pounds for the year, and what are the average yearly earnings that you expect of your insurance company?

Suppose claims are arriving at your insurance company at a rate of λ > 0, meaning that the total number of claims Nt that have arrived by time t is a Poisson process with intensity λ. These claims are not handled immediately, but are instead collected in a queue. At random times T1, T2, . . . all the claims currently in the queue are dealt with and so the queue is reset to zero. The waiting times between resets of the queue, namely Sk := Tk −Tk−1, are assumed to be i.i.d. with Sk ∼ Exp(γ) for some γ > 0. We are interested in understanding the continuous time Markov chain (Xt)t≥0, where Xt is the number of claims in the queue at time t (currently waiting to be dealt with) starting from X0 = 0.

(a) [3 marks] Identify the Q matrix of (Xt)t≥0, by specifying the entries Q(i, j) for all i, j in the state space. Briefly explain why the entries are the way they are.

(g) [3 marks] Derive the limits of pt(0) and pt(1) as t → ∞. Explain how this relates to (d), by referring to a theorem from lectures (very briefly explaining why the assumptions are satisfied). In the long run, what proportion of the time do we expect there to be precisely 1 claim waiting to be dealt with?

更多代写:c code辅导 ielts indicator作弊 英国统计信息管理网课代考 论文查重英文怎么说 apa参考文献 论文写不出

合作平台:essay代写 论文代写 写手招聘 英国留学生代写

Math 632 - Midterm Exam 数学马尔科夫链代写 • There are six problems on the exam, and they have multiple parts. The total number of points is 100. • Your solutions must be fully uploaded • Th...

View details

Statistics 1 Duration: 1h:30m exam统计代考 Note: During the test only the use of a sheet with formulas and a calculator areallowed. QUESTION 1 (5,0) Punctuality in meetings is a worrying ...

View details

Statistics I Exam – 2nd sitting 统计exam代写 Please be reminded to define all the relevant random variables and quantities and justify your answers carefully. Please be reminded to defi...

View details

W6: Weekly quiz 统计quiz代考 Quiz Instructions This quiz will cover the asynchronous content from the Week 6 module. It is due BEFORE our synchronous class. Quiz Instructions This quiz ...

View details