管理会计代写 MANAGEMENT ACCOUNTING代写 会计代写

985BUSN7031: MANAGEMENT ACCOUNTING Practice Questions 管理会计代写 1. ABC has determined that the shipment setup costs should be accounted for at the batch-level of activities. ABC believes tha...

View detailsSearch the whole station

财务会计代写 INFORMATION 1.The duration of the exam is 2 hours and 30 minutes. 2.The exam must be performed individually. 3.Only calculators with simple

Multiple Choice Questions (6.0 points)

From a financial accounting regulations and practice standpoints, only one of the answers to each of the ten questions below is possible.

An intangible asset

a. derives its value from the rights and privileges it provides the owner.

b. is worthless because it has no physical substance.

c. is converted into a tangible asset during the operating cycle.

d. cannot be classified on the balance sheet because it lacks physical substance.

e. None of the above.

Which statement about long-term investments is not true?

a. They will be held for more than one year.

b. They are not currently used in the operation of the business.

c. They include investments in stock of other companies and land held for future use.

d. They do not include long-term notes receivable.

e. None of the above.

These are selected account balances on December 31, year N:

Land $100,000

Land (held for future use) 150,000

Buildings 800,000

Inventory 200,000

Equipment 450,000

Furniture 100,000

Accumulated Depreciation 300,000

What is the total amount of property, plant, and equipment that will appear on the balance sheet?

a. $1,500,000

b. $1,300,000

c. $1,800,000

d. $1,150,000

e. None of the above.

Dawson Corporation has the following information available for year N:

| (in millions) | |

| Issued ordinary shares | $45 |

| Treasury ordinary shares | $65 |

| Paid dividends | $75 |

| Net income | $130 |

| Beginning Share Capital Ordinary balance | $625 |

| Beginning Retained Earnings balance | $475 |

Based in this information, what is Dawson’s Share Capital Ordinary balance at the end of the year?

a. $605

b. $735

c. $245

d. $680

e. None of the above

What is the relationship between present value and the concept of a liability?

a. Present values are used to measure certain liabilities.

b. Present values are not used to measure liabilities.

c. Present values are used to measure all liabilities.

d. Present values are only used to measure non-current liabilities.

e. None of the above.

What is a purpose of having a conceptual framework?

a. To enable the profession to more quickly solve emerging practical problems.

b. To provide a foundation from which to build more useful standards.

c. Neither a nor b.

d. Both a and b.

e. None of the above.

Which of the following is a fundamental quality of useful accounting information?

a. Conservatism.

b. Comparability.

c. Faithful representation.

d. Consistency.

e. None of the above.

The amount of the liability for compensated absences should be based on

1. the current rates of pay in effect when employees earn the right to compensated absences.

2. the expected rates of pay expected to be paid when employees use compensated time.

3. the present value of the amount expected to be paid in future periods.

a. 1.

b. 2.

c. 3.

d. Either 1 or 2 is acceptable.

e. None of the above.

Which of the following terms is associated with recognizing a provision?

a. Possible but not probable.

b. Likely.

c. Remote.

d. Probable.

e. None of the above.

Information available prior to the issuance of the financial statements indicates that it is probable that, at the date of the financial statements, a company has a present obligation related to product warranties. The amount of the expense involved can be reasonably estimated. Based on the above facts, the estimated warranty expense should be

a. accrued.

b. disclosed but not accrued.

c. neither accrued nor disclosed.

d. classified as an appropriation of retained earnings.

e. None of the above.

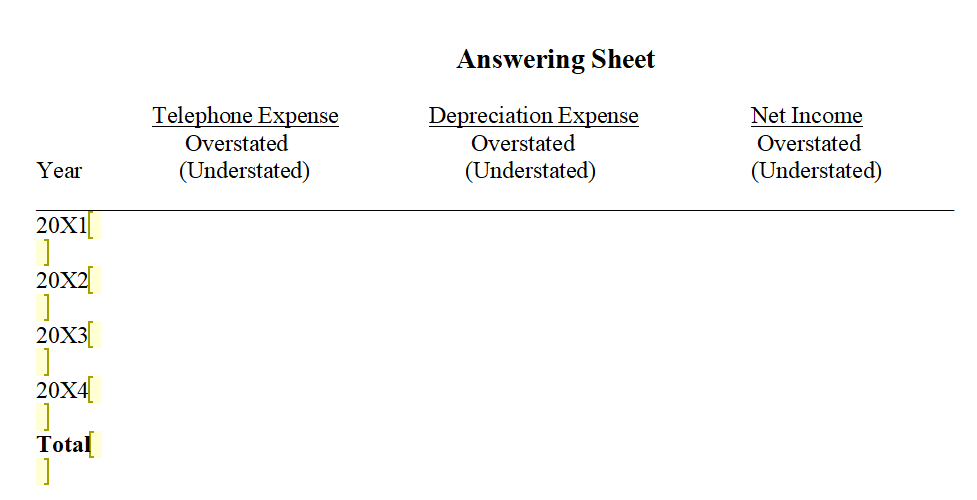

On January 1, 20X0 Marvel Company purchased and installed a telephone system at a cost of ₤20,000. The equipment was expected to last five years with a residual value of ₤3,000. On January 1, 20X1 more telephone equipment was purchased to tie-in with the current system for ₤10,000. The new equipment is expected to have a useful life of four years. Through an error, the new equipment was debited to Telephone Expense. Marvel Company uses the straight-line method of depreciation.

Required:

Fill in the schedule below showing the effects of the error on Telephone Expense, Depreciation Expense, and Net Income for each year and in total beginning in 20X1 through the useful life of the new equipment.

During the current year, Penny Company incurred several expenditures. Briefly explain whether the expenditures listed below should be recorded as an operating expense or as an intangible asset. If you view the expenditure as an intangible asset, indicate the number of years over which the asset should be amortized. Explain your answer.

(a) Spent $30,000 in legal costs in a patent defense suit. The patent was unsuccessfully defended.

(b) Purchased a trademark from another company. The trademark can be renewed indefinitely. Penny Company expects the trademark to contribute to revenue indefinitely.

(c) Penny Company acquires a patent for $2,000,000. The company selling the patent has spent $1,000,000 on the research and development of it. The patent has a remaining life of 15 years.

(d) Penny Company is spending considerable time and money in developing a different patent for another product. So far $3,000,000 has been spent this year on research. Penny Company is very confident they will obtain this patent in the next few years.

Harrington Company reported the following balances at December 31, 20X0: share capital–ordinary $500,000; share premium–ordinary $100,000; retained earnings $250,000. During 20X1, the following transactions affected equity.

1. Issued preference shares with a par value of $150,000 for $200,000.

2. Purchased treasury shares (ordinary) for $40,000.

3. Earned net income of $140,000.

4. Declared and paid cash dividends of $75,000.

Required:

Prepare the equity section of Harrington Company’s December 31, 20X1, statement of financial position.

Rosen Company purchased 35,000 ordinary shares of Polo Corporation as a long-term investment for ₤700,000. During the year, Polo Corporation reported net income of ₤300,000 and paid dividends of ₤100,000.

Required:

(a) Assuming that the 35,000 shares represent a 10% interest in Polo Corporation:

1. Prepare the journal entry to record the investment in Polo.

2. Prepare any entries that Rosen Company should make in accounting for its investment in Polo during the year.

3. What is the balance of the Share Investments account on Rosen Company’s books at the end of the year?

(b) Repeat requirement (a) above except assume that the 35,000 shares represent a 35% interest in Polo Corporation.

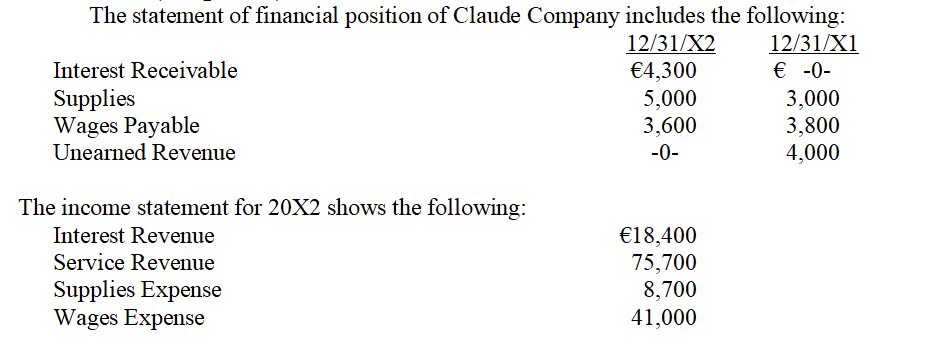

Required:

Calculate the following for 20X2:

1. Cash received for interest.

2. Cash paid for supplies.

3. Cash paid for wages.

4. Cash received for revenue.

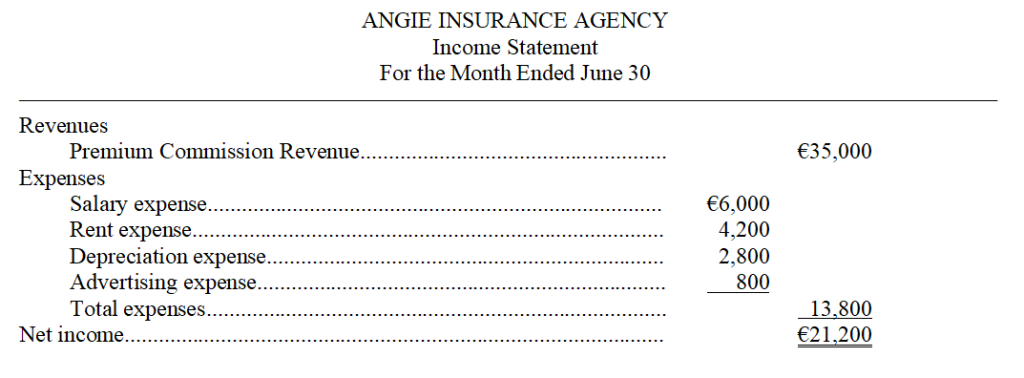

Angie Insurance Agency prepares monthly financial statements. Presented below is an income statement for the month of June that is correct on the basis of information considered.

Additional Data:

When the income statement was prepared, the company accountant neglected to take into consideration the following information:

1. A utility bill for €2,000 was received on the last day of the month for electric and gas service for the month of June.

2. A company insurance salesman sold a life insurance policy to a client for a premium of €25,000. The agency billed the client for the policy and is entitled to a commission of 20%.

3. Supplies on hand at the beginning of the month were €3,000. The agency purchased additional supplies during the month for €3,500 in cash and €1,200 of supplies were on hand at June 30.

4. The agency purchased a new car at the beginning of the month for €24,000 cash. The car will depreciate €6,000 per year.

5. Salaries owed to employees at the end of the month total €5,300. The salaries will be paid on July 5.

Required:

Prepare a correct income statement.

Prepare the required end-of-period adjusting entries for each independent case listed below.

Case 1

Moon Company began the year with a $3,000 balance in the Office Supplies account. During the year, $8,500 worth of additional office supplies were purchased. A physical count of office supplies on hand at the end of the year revealed that $6,400 worth of office supplies had been used during the year. No adjusting entry has been made until year end.

Case 2

West Company has a calendar year-end accounting period. On July 1, the company purchased office equipment for $30,000. It is estimated that the office equipment will depreciate $500 each month. No adjusting entry has been made until year end.

Case 3

Ruth Realty is in the business of renting several apartment buildings and prepares monthly financial statements. It has been determined that 3 tenants in $700 per month apartments and one tenant in the $1,000 per month apartment had not paid their August rent as of August 31st.

更多代写:CS网课代修 GMAT代考 英国Game Theory博弈论代上网课 芝加哥essay代写 瑞士留学生论文代写 网课代修机构推荐

合作平台:essay代写 论文代写 写手招聘 英国留学生代写

BUSN7031: MANAGEMENT ACCOUNTING Practice Questions 管理会计代写 1. ABC has determined that the shipment setup costs should be accounted for at the batch-level of activities. ABC believes tha...

View details

Final Exam 财务会计期末代考 Question 2 Everest Foam Company (EFC) has developed and manufactured a foam mattress which is proven to last for 10 years. Question 1 Given the following i...

View details

AC.F 304 ACCOUNTING AND FINANCE 会计金融市场代写 FINANCIAL MARKETS (DURATION: 2.5 HOURS plus 30 minutes upload time) This examination paper consists of four sections. All Sections (A, B, C and ...

View details

FINANCIAL ACCOUNTING II Mid-term Multiple-choice questions 财务会计考试助攻 1. Which of the following is a characteristic describing the primary quality of relevance? A. Materiality. B. ...

View details